SEC Adopts Significant Amendments to Improve Financial Disclosures Regarding Business Acquisitions and Dispositions

In an attempt to improve the financial information presented to investors in connection with many M&A transactions, the United States Securities and Exchange Commission (the “SEC”) recently adopted highly anticipated amendments to Regulation S-X (“Reg. S-X”) under the Securities Act of 1933, as amended.

In summary, these amendments:

- align the significance thresholds used in dispositions with the minimum significance thresholds used for acquisitions;

- revise the tests commonly utilized by registrants to test the significance of a business acquisition or disposition;

- reduce the maximum number of years of financial statements required for significant business acquisitions to two years (even at the highest levels of significance);

- change the types of pro forma adjustments a registrant is permitted to make when preparing and presenting pro forma financial information;

- expand the use of pro forma financial information in evaluating significance;

- revise the disclosure requirements for individually insignificant acquisitions; and

- make a number of other technical changes to the requirements for significant business acquisitions and dispositions.

Although these amendments do not take effect until January 1, 2021, the SEC will permit registrants to voluntarily comply with them prior to such date so long as the amendments are applied in their entirety.

Adopted SEC amendments in this alert:

- Alignment of Significance Levels Related to Dispositions

- Amended Significance Tests

- Reduced Financial Statement Disclosure Obligations

- Changes to Pro Forma Financial Information

- Expanded Use of Pro Forma Financial Information in Measuring Significance

- Revisions to the Treatment of Individually Insignificant Acquisitions

- Other Technical Amendments

Alignment of Significance Levels Related to Dispositions

The current rules require registrants to file pro forma financial statements to reflect significant business dispositions. The significance threshold for dispositions currently differs from the threshold used for acquisitions. While an acquisition is not deemed significant unless it passes a 20% significance threshold, the current rules use a 10% significance threshold for dispositions. The amendments raise the significance threshold for dispositions from 10% to 20%.

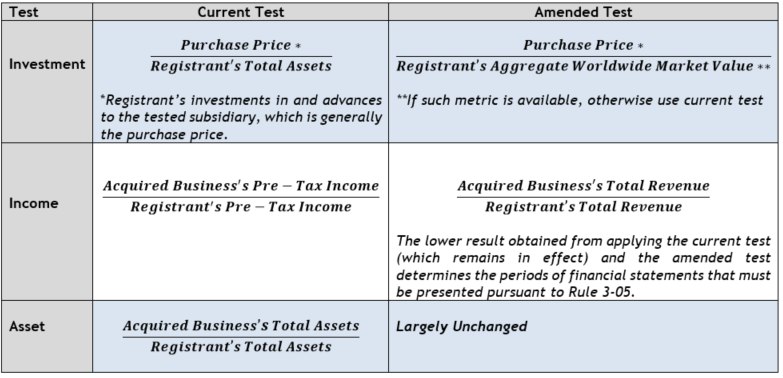

Amended Significance Tests

To evaluate the significance of a business acquisition or disposition, registrants apply three tests, which are commonly referred to as the investment, income and asset tests. These three tests measure significance as a percentage by comparing various aspects of the acquired business to that of the registrant. No one test is more important than the others, and the highest percentage yielded from applying these three tests is used for purposes of determining whether, and to what extent, financial statements of the acquired business will be necessary.

The chart below compares and contrasts the current versions of these three tests with the amended versions.

Investment Test

Current Test

The investment test currently compares (i) the registrant’s (and its subsidiaries’) investment in and advances to the acquired or disposed business to (ii) the total assets of the registrant as of its most recently completed fiscal year. The numerator is generally the consideration transferred or received (i.e., the purchase price) for the assets being acquired or sold.

Amended Test

Under the amended investment test, registrants will instead use their aggregate worldwide market value[1] as the denominator when assessing the significance of business acquisitions or dispositions. However, if the registrant does not have an aggregate worldwide market value, it must continue to use the current version of the investment test. In addition, the amendments clarify that the revised investment test is only applicable when measuring the significance of acquisitions and dispositions. Therefore, when registrants evaluate the significance of their subsidiaries, the investment test remains unchanged.

To calculate the aggregate worldwide market value, registrants will use the last five trading days of their most recently completed month ending prior to the earlier of (i) the date the acquisition or disposition agreement is signed or (ii) the date the transaction is announced.

The amendments clarify that the registrant’s (and its subsidiaries’) investments in the acquired or disposed business must include the fair value of contingent consideration if such consideration is required to be recognized at fair value by the registrant at the acquisition date under U.S. generally accepted accounting principles (“U.S. GAAP”) or IFRS as issued by the International Accounting Standards Board (“IFRS-IASB”), as applicable. If the registrant is not required to recognize the contingent consideration at fair value, the registrant must include all contingent consideration unless the likelihood such contingent consideration will be paid is remote.

SEC’s Rationale

One of the SEC’s stated rationales for revising the investment test (in certain contexts) was to more closely align the metric used in the denominator with the purchase price metric used in the numerator. Purchase price is generally consistent with fair market value, but total assets are often reflected based on book value, which frequently does not reflect the current fair market value of the registrant’s assets. Using the aggregate worldwide market value helps to address this mismatch since the value is determined by the market. In addition, the SEC believed that using a more recent measurement period that is averaged to help adjust for daily variability would provide a more accurate baseline for registrants to use when determining the significance of an acquisition or disposition. In addition, the SEC believed that requiring the inclusion of contingent consideration would provide a more accurate measure of the acquired business’s potential significance while also helping to mitigate the risk of under-identifying significant acquisitions for which Rule 3-05 Financial Statements are necessary to reasonably inform investors.

Income Test

Current Test

The current version of the income test compares (i) the registrant’s (and its subsidiaries’) equity in the income from continuing operations (pre-tax and exclusive of amounts attributable to any non-controlling interests) of the acquired or disposed business in its most recently completed fiscal year to (ii) the same measure of the registrant (and its subsidiaries) in its most recently completed fiscal year.

Amended Test

The amendments introduce a revenue component to the income test to help reduce anomalous results, especially for registrants with marginal or break-even income in recent fiscal years. The newly created revenue test compares (i) the acquired or disposed business’s total consolidated revenue (after intercompany eliminations) from continuing operations to (ii) the registrant’s consolidated revenue from continuing operations in its most recently completed fiscal year. In order to use the new revenue component of the income test, both the acquired or disposed business and the registrant must have had material revenue in each of their two most recently completed fiscal years.

In order to be significant under the revised income test, the business acquisition or disposition must now meet both the net income component and the new revenue component (when the revenue component applies), and, for purposes of applying Rule 3-05 of Reg. S-X, registrants may use the lower of the revenue component and the net income component. In other words, the income test is met at certain significance levels only if both the net income and the revenue components pass the significance thresholds. If both components are met, the lower of the two percentages is used for purposes of determining the periods of financial statements of the acquired business that are required (hereinafter referred to as “Rule 3-05 Financial Statements”).

Absolute Values

The amendments further clarify that, if either the registrant or the acquired or disposed business had a net loss, the net income portion of the income test will be based on absolute values.

SEC’s Rationale for Amending the Income Test

Revenue is an important business indicator and is generally less variable than net income. Including a revenue component will reduce the frequency in which immaterial acquisitions pass a significance threshold under this test for purposes of Rule 3-05 of Reg. S-X.

Asset Test

The current asset test compares (i) the total assets reflected in the acquired business’s most recent annual pre-acquisition financial statements to (ii) the same metric in the registrant’s business. The new amendments did not make any substantive changes to the asset test.

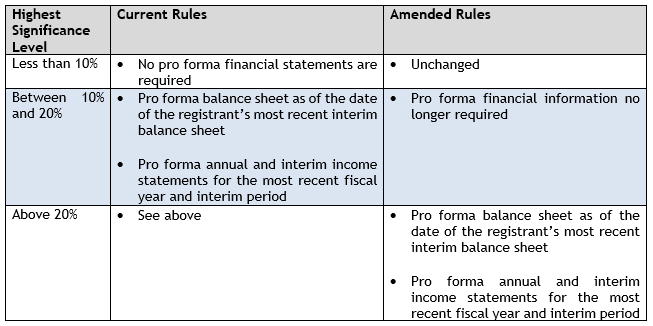

Reduced Financial Statement Disclosure Obligations

After assessing the significance of a potential business acquisition or disposition under each of the three tests outlined above, registrants use the highest percentage yielded under these tests to determine the scope of the required Rule 3-05 Financial Statements and pro forma financial information.

The charts below provide a high level comparison of the registrant’s financial disclosure obligations under the current and amended rules in connection with business acquisitions and dispositions.

Financial Disclosure Obligations in Connection with Business Acquisitions

Financial Disclosure Obligations in Connection with Business Dispositions[3]

SEC’s Rationale

As the charts above illustrate, one of the most significant changes implemented by these amendments is the decrease in the number of years of Rule 3-05 Financial Statements required at the highest levels of significance. No commenters opposed this reduction, and the amendments will offer welcome relief to registrants from the burdens and costs associated with obtaining an audit on an acquired business’s third year of pre-acquisition financial statements.

The SEC rationalized that because (i) the third year of acquired business financials is much less illustrative of the acquired business’s current financial condition and (ii) the acquired business’s financial statements are supplemented with pro forma financial information, the benefits associated with requiring such disclosure were outweighed by the burdens.

However, the SEC cautioned that, if the trends depicted in the Rule 3-05 Financial Statements are not indicative of the current financial condition or are otherwise incomplete, the registrant is obligated to provide “such further material information as is necessary to make the required statements, in light of the circumstances in which they are made, not misleading.”

Changes to Pro Forma Financial Information

Pro forma financial information in connection with a business acquisition essentially combines the historical financial statements of the acquired business and the registrant. This pro forma financial information is intended to give investors an idea of what the combined businesses would have looked like historically and to illustrate the impact of the transaction on the financial position of the registrant.

Current Rules

The current rules permit registrants to make certain limited adjustments to the pro forma financial information. For example, registrants may make adjustments to their pro forma income statements if such adjustments are (i) directly attributable to the transaction, (ii) expected to have a continuing impact on the registrant and (iii) factually supportable. In addition, the registrant may make adjustments to its pro forma balance sheet to reflect adjustments that are (x) factually supportable and (y) directly attributable to the transaction.

Amended Rules

In adopting the proposed amendments, the SEC acknowledged that the pro forma adjustment criteria under the current rules are not clearly defined, potentially yield inconsistent presentations and preclude adjustments related to the potential effects of post-acquisition actions. The amendments completely replace the existing pro forma adjustment criteria with simplified requirements that are broken down into three categories: (i) Transaction Accounting Adjustments, (ii) Autonomous Entity Adjustments and (iii) Management’s Adjustments.

- Transaction Accounting Adjustments are required adjustments that reflect only the application of required accounting to the transaction linking the effects of the acquired business to the registrant’s audited historical financial statements.

- Autonomous Entity Adjustments are required adjustments that are necessary to reflect the operations and financial position of the registrant as an autonomous entity when the registrant was previously part of another entity.

- Management’s Adjustments are optional adjustments that provide registrants with some flexibility to (i) include forward-looking information depicting the synergies and dis-synergies identified by management in determining whether to consummate or integrate the transaction and (ii) provide insight to investors into the potential effects of the acquisition and the post-acquisition plans expected to be taken by management.

Management’s Adjustments must (i) have a reasonable basis, (ii) be limited to the effect of synergies and dis-synergies as if they existed as of the beginning of the fiscal year presented and (iii) must reflect all adjustments that management believes are necessary in order to fairly state the pro forma financial information presented.

In addition, Management’s Adjustments must (i) be presented in the explanatory notes to the pro forma financial statements, (ii) be presented as of the most recent practicable date prior to the effective date, mail date, qualified date or filing date, as applicable, if included in any registration statement, proxy statement, offering document or Form 8-K (which may require that they be updated if previously provided in a Form 8-K that is appropriately incorporated by reference), (iii) present any modifications to the number or potential number of common shares as if they existed as of the beginning of the fiscal year presented and (iv) include the basis and material limitations of each adjustment.[4]

Expanded Use of Pro Forma Financial Information in Measuring Significance

Current Rules

When measuring the significance of a business acquisition, registrants generally compare the most recent annual financial statements of the acquired business with the registrant’s most recent annual financial statements. However, under certain limited circumstances, registrants are permitted to use pro forma, rather than the most recent annual, financial statements to test significance. Under the current rules, in order to rely on pro forma financial information, the registrant must have (i) made a significant business acquisition subsequent to its last fiscal year and (ii) filed the required pro forma financial information related on that acquisition on a Form 8-K. This current Form 8-K filing prerequisite effectively prevents a non-reporting registrant that is filing an initial registration statement from using pro forma financial information to measure significance.

Amended Rules

The amendments abolish the requirement that such pro forma financial information be filed on Form 8-K and permit registrants to use the pro forma financial information to test significance as long as the registrant has filed (i) the Rule 3-05 Financial Statements and (ii) the pro forma financial information required by Article 11 of Reg. S-X. However, the pro forma financial information used to measure significance may not give effect to Autonomous Entity Adjustments or Management’s Adjustments.

The amendments also codify existing practice by requiring a registrant that uses pro forma financial information to continue to test the significance of any subsequent acquisitions using pro forma financial information until the registrant files its next annual report.

Revisions to the Treatment of Individually Insignificant Acquisitions

Current Rules

The current rules governing individually insignificant acquisitions do not generally require a registrant to provide pro forma financial information, except when the acquisitions, in the aggregate, exceed a 50% significance threshold based on the registrant’s latest audited balance sheet. In these circumstances, the registrant is required to provide Rule 3-05 Financial Statements and corresponding pro forma financial information for the “substantial majority” of the individually insignificant acquisitions in any registration or proxy statement that it files.

Substantial majority has been interpreted as requiring any combination of individually insignificant acquisitions that adds to a mathematical majority. For example, if a registrant completed 12 acquisitions, each with a 5% significance level, since filing its last audited financial statements, then, in the aggregate, those individually insignificant acquisitions would have a significance level of 60%. Under the substantial majority standard, the registrant would need to provide Rule 3-05 Financial Statements for any 7 of those acquisitions, and the pro forma financial information the registrant files would illustrate the impact of those 7 acquisitions (amounting to 35% of the registrant’s pre-acquisition assets or income).

Amended Rules

The amendments clarify that “individually insignificant” acquisitions include the following: (i) acquisitions consummated after the registrant’s audited balance sheet date whose significance does not exceed 20%, (ii) any probable acquisition whose significance does not exceed 50% and (iii) any consummated acquisition whose significance is between 20% and 50%, and for which the otherwise required Rule 3-05 Financial Statements (and pro forma financial information) has not been filed because of the 71 day grace period provided in Form 8-K.

The amendments also revise the financial disclosure obligations for registrants related to individually insignificant acquisitions. Under the amended rules, a registrant’s registration and proxy statements are only required to include Rule 3-05 Financial Statements for acquisitions that exceed 20%. However, the pro forma financial information must show the aggregate effects of all individually insignificant acquisitions in all material respects.

Other Technical Amendments

The amendments also contain a number of technical changes, including the following:

- Flexibility Regarding Which Form 10-K to Use: Currently, a registrant must use the financial information contained in its most recent Form 10-K to measure the significance of a business acquisition or disposition, even when the most recent Form 10-K was filed after the acquisition date. Under the amendments, in the event the registrant files its Form 10-K after the acquisition date but prior to the date when the Rule 3-05 Financial Statements are due, the registrant is permitted to use either its most recent Form 10-K or its Form 10-K from the prior year to compute significance.[5]

- Ability to Reconcile to International Financial Reporting Standards: The amendments permit foreign private issuers that prepare their financial statements in accordance with IFRS-IASB to reconcile the Rule 3-05 Financial Statements in connection with the acquisition of a foreign business that prepares its financial statements using home country GAAP to IFRS-IASB (as opposed to U.S. GAAP). In addition, if the acquired business would have qualified to report its financial statements under IFRS-IASB had it been a registrant, the amendments permit the registrant to prepare the Rule 3-05 Financial Statements in accordance with IFRS-IASB without including a reconciliation to U.S. GAAP.

- Omission of Rule 3-05 Financial Statements After Certain Periods of Time: The amendments no longer require the inclusion of Rule 3-05 Financial Statements in a registrant’s registration and proxy statements once the acquired business is reflected in the registrant’s financial statements for specified periods of time.

- For business acquisitions between 20% and 40% significance, registrants may omit the Rule 3-05 Financial Statements after nine months.

- For business acquisitions above 40% significance, registrants may omit the Rule 3-05 Financial Statements after a complete fiscal year.

- Abbreviated Financial Statements for Acquisitions of Components of an Entity: The amendments permit registrants that acquire a component of an entity to, in certain limited circumstances, provide specified abbreviated financial statements for the acquired business. For this relief to apply, (i) the total assets and revenues (each after intercompany eliminations) of the acquired business must represent less than 20% of the total consolidated assets and revenues, respectively, of the seller as of the end of and for the most recently completed fiscal year; (ii) the acquired business must not be a separate entity, subsidiary, operating segment or division; (iii) separate financial statements for the business must not have been previously prepared; and (iv) the seller must not have maintained the separate and distinct accounts necessary to present financial statements and it must be impracticable to prepare such financial statements.

The rules governing the disclosure obligations of public companies are complex and fact and circumstance specific. If you have any questions related to this alert, please do not hesitate to contact any member of the Public Companies group or your regular Smith Anderson lawyer.

[1] Aggregate worldwide market value for purposes of this test differs from the aggregate worldwide market value metric utilized to determine filing status and eligibility to use registration statements on Form S-3. Under the amended investment test, the aggregate worldwide market value (i) includes the value of common equity held by affiliates and (ii) is based on the average worldwide market value during the last five trading days in the most recently completed month ending prior to the earlier of (a) the announcement date of the transaction or (b) the date the acquisition or disposition agreement is signed. In contrast, when registrants assess their filing status, the aggregate worldwide market value (x) is measured on the last day of the registrant’s most recently completed second fiscal quarter and (y) only takes into account the voting and non-voting common equity held by its non-affiliates. Calendar year end public companies currently preparing to begin work on their second quarter Form 10-Qs are reminded to test their filing status as of June 30, 2020.

[2] Under the current rules, registrants may omit the third year of acquired business financial statements if the net revenues reported by the acquired business in its most recent fiscal year are less than $100 million.

[3] Dispositions of a significant business do not require the presentation of historical financial statements for the business in question. However, significant business dispositions do require the presentation of pro forma financial information. As a reminder, registrants must file the pro forma financial statements in connection with significant business dispositions within 4 business days. The 71 day grace period available for acquisitions does not extend to dispositions. Late filings under Item 2.01 of Form 8-K will impact a registrant’s eligibility to use short form registration statements on Form S-3, which in turn can hinder the registrant’s ability to quickly conduct registered offerings of securities to raise capital.

[4] The procedures auditors use in connection with providing negative assurance comfort on pro forma financial information are based on the current formulation of the pro forma rules in Article 11 of Reg. S-X. As such, companies are encouraged to allocate additional time to interact with auditors in connection with obtaining comfort on any pro forma financial statements prepared using the new standards.

[5] Registrants may request permission from the SEC to waive certain financial disclosure requirements under Rule 3-13 of Reg. S-X if the registrant believes the financial information would be burdensome to generate and immaterial to investors. SEC Chairman Jay Clayton has encouraged registrants to consider making such requests, and the current SEC staff is placing a high priority on responding to these waiver requests with timely guidance.

Professionals

Attorney

Attorney Attorney

Attorney Attorney

Attorney